The contribution margin is computed as the selling price per unit, minus the variable cost per unit. Also known as dollar contribution per unit, the measure indicates how a particular product contributes to the overall profit of the company. If your total fixed production expenses were $300,000, you’d end up with ($50,000) in net profit ($250,000-$300,000). This is a loss, so you’d have to figure out how to compensate for the -$50,000 by increasing sales or decreasing fixed costs. For that, you’ll need a tool that automates data collection, accurately calculates financial insights, and produces customizable reports.

Contribution Margin Ratio FAQs

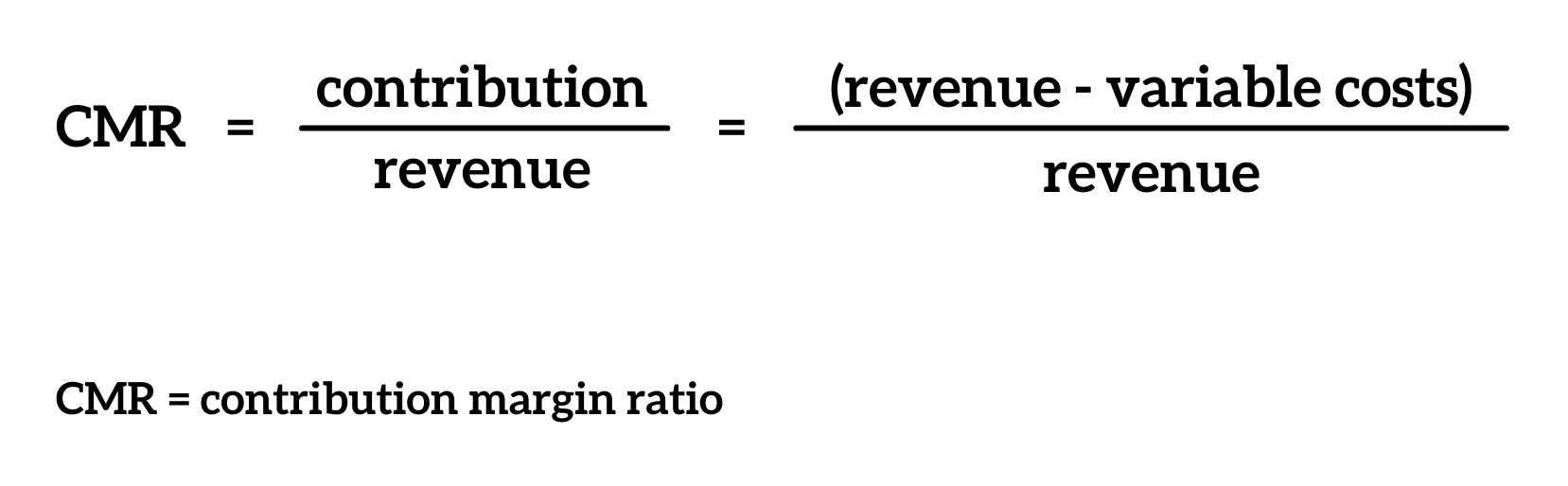

It is important for you to understand the concept of contribution margin. This is because the contribution margin ratio indicates the extent to which your business can cover its fixed costs. The “contribution income statement” is a special recipe to see how sweet your lemonade sales are. A business can increase its Contribution Margin Ratio by reducing the cost of goods sold, increasing the selling price of products, or finding ways to reduce fixed costs. In the United States, similar labor-saving processes have been developed, such as the ability to order groceries or fast food online and have it ready when the customer arrives. Do these labor-saving processes change the cost structure for the company?

What other financial metrics are related to the Contribution Margin Ratio?

While contribution margins only count the variable costs, the gross profit margin includes all of the costs that a company incurs in order to make sales. Also important in CVP analysis are the computations of contribution margin per unit and contribution margin ratio. In our example, the sales revenue from one shirt is $15 and the variable cost of one shirt is $10, so the individual contribution margin is $5. This $5 contribution margin is assumed to first cover fixed costs first and then realized as profit. As mentioned above, contribution margin refers to the difference between sales revenue and variable costs of producing goods or services.

Analysis of the Contribution Margin Income Statement

From contribution margin figure all fixed expenses are subtracted to obtain net operating income. The following simple formats of two income statements can better explain this difference. Conversely, a lower contribution margin ratio may indicate a significant portion of sales revenue is consumed by variable costs, leaving less to cover fixed costs and contribute to profit.

Understanding the Impact of Variable Costs

- The contribution margin and the variable cost can be expressed in the revenue percentage.

- It does not matter if your expenses are production or selling and administrative expenses.

- And finally, the gross margin is replaced in the statement by the contribution margin.

- In this section, we’re going to learn how to figure out something called the contribution margin.

Fixed costs are often considered sunk costs that once spent cannot be recovered. These cost components should not be considered while making decisions about cost analysis or profitability measures. Before you begin your calculations, you’ll need to understand fixed and variable expenses.

Insights into Product Profitability

By incorporating contribution margin insights into the decision-making process, finance professionals better understand how different aspects of the business contribute to overall profitability. Armed with contribution margin insights, businesses are empowered to make strategic decisions that drive sustainable business growth. Whether it’s introducing new products, entering new markets, or optimizing existing processes, the ability to assess potential outcomes through the contribution margin lens enhances decision-making accuracy. Businesses chart a course for long-term success upon aligning actions with profitability goals. In effect, the process can be more difficult in comparison to a quick calculation of gross profit and the gross margin using the income statement, yet is worthwhile in terms of deriving product-level insights.

This \(\$5\) contribution margin is assumed to first cover fixed costs first and then realized as profit. The Indirect Costs are the costs that cannot be directly linked to the production. Indirect materials and indirect labor costs that cannot be directly allocated to your products are examples of calculating profits and losses of your currency trades indirect costs. Furthermore, per unit variable costs remain constant for a given level of production. The contribution margin income statement separates the fixed and variables costs on the face of the income statement. This highlights the margin and helps illustrate where a company’s expenses.

Watch this video from Investopedia reviewing the concept of contribution margin to learn more. Keep in mind that contribution margin per sale first contributes to meeting fixed costs and then to profit. Profit margin is calculated using all expenses that directly go into producing the product. The contribution margin income statement is a useful tool when analyzing the results of a previous period.

Last month, Alta Production, Inc., sold its product for $2,500 per unit. Fixed production costs were $3,000, and variable production costs amounted to $1,400 per unit. Fixed selling and administrative costs totaled $50,000, and variable selling and administrative costs amounted to $200 per unit.